15 minutes agoAuthor: Gaurav Tiwari

- Copy link

Diwali The festival of lights seems incomplete without lights, sweets and shopping. At this time there is a glut of offers and discounts everywhere in the market. Most offers in it are available on credit cards. In such a situation, most people use credit cards to shop.

This makes it easier to pay and provides cashback and rewards in a large amount. However, many times people spend excessively due to this facility. When the bill comes out, its burden becomes a headache. In such a situation, the joy of Diwali turns into debt and stress.

Actually, the correct use of credit card also gives you benefits and misuse can also implicate you in a debate trap. In such a situation, it is important that some care should be taken while shopping and a plan should be made in advance.

So today we ‘Your moneyIn the column, you will know that-

- How to use credit card during Diwali shopping?

- How to avoid credit card debt trap?

- If you are in a debate trap, what is the easy way to get out?

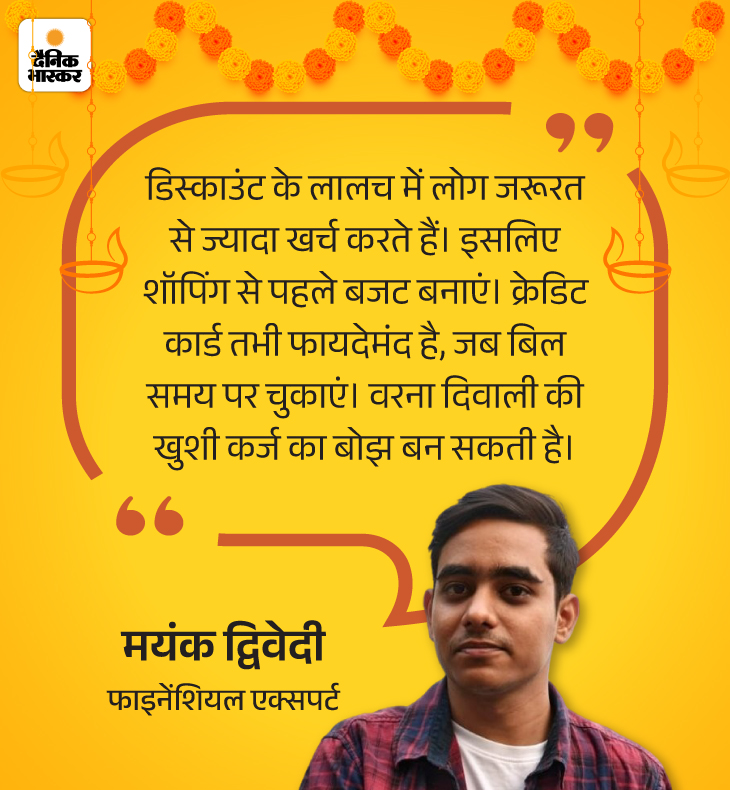

Question- How beneficial the credit card offers are and what precautions should be taken during their use?

answer- Credit card companies and banks offer attractive offers and discounts on Diwali. These include cashback, no-cost EMI and bonus rewards. If you do shopping by planning and making budgets in advance, then with the help of these offers, you can do big shopping at less expenses.

However, spending excessively in the name of these offers is the biggest mistake. Let us understand what precautions should be taken during the use of credit cards, through graphic.

Question- How much is it right to use a credit limit while shopping?

answer- Credit limit is never intelligent to spend the whole. Experts believe that you should use only 30–40% of your total credit limit. This not only keeps your CIBIL score better, but it is also easy to pay the bill.

Question- Why should you avoid cash withdrawal on credit card at the time of shopping?

answer- Withdrawal of cash from credit card is the most expensive deal. Interest starts immediately, while on shopping you get an interest-free period of 30 to 50 days. Apart from this, cash advance fees are charged up to 2–3% as soon as the cash is withdrawn from ATM. That is, you will have to pay more than the money withdrawn.

Question- How much debt is there more debt?

answer- An easy way to understand your financial health is Debt-to-Income (DTI) ratio. That is, how much of the income that is made every month goes to repaying the loan or EMI. If this part is less then it is fine, but if it becomes more than 50%, then it can increase difficult. Home loan banks want it to be less than 36%.

The second way is the credit utilization ratio- Meaning, how much you are spending compared to your credit card limit. If you use too much part of the limit, the credit score can be spoiled. Banks believe that 30%of the credit limit should not be used more than 30%-40.

Question- How much damage can be caused if the credit card bill is not repaid on time?

answer- If you do not repay the credit card bill on time, the banks charge an annual interest of up to 30-45% annually. This rate is much higher than any personal loan. Not only this, late payment charge and GST are added separately. By repeated delays, your CIBIL score gets spoiled, which can make it difficult to take a loan in the future.

Question- What smart steps can be adopted to manage credit card bill after Diwali?

answer- After Diwali, you can adopt some ways to manage credit card bills. For example, to avoid credit card debt, first make a list by writing the expenses of the entire month. It will be clearly visible that where more money is being spent. It is necessary to brake immediately on non-essential expenses. If you get a bonus or any extra income, then use it directly in credit card payment. Set the auto-deduction to cut the bill on time. And if possible, avoid shopping or luxury expenses by next month, so that the debt burden can be reduced quickly.

Question- If excessively spent on Diwali, then how can the debate be avoided?

answer- First of all, never spend more than your capacity. This habit can trap you in a debt trap. Credit card car can take you on the path of Kangali. Let us understand it through graphic.

Question- When should the balance transfer and EMI option of credit cards be taken?

answer- Balance transfer should be taken when your bill is too much and you are not in a position to pay all the dues on a card. In such a situation, you can transfer balance to a card with low interest rate. The EMI option is correct when the expenditure is big, but you can gradually repay it comfortably in installments.

- Balance transfer when there is a loan of more than one card.

- EMI option is better for large expenses, such as electronics, jewelry.

- Before taking EMI, see processing fees and interest rates.

Question- What mistakes should be avoided once after recovering from credit card debt? So that the debent does not get stuck in the trap again.

answer- To avoid increasing credit card debt, it is necessary to make a budget first, so that you can manage your income and expenses correctly.

Also understand why you spend excessively, because recognizing your feelings is easy to control wasteful. Try to make most of the payment with cash and if you have to use the credit card, then pay the entire bill every month.

Close the forest-click bing and put the details of the card every time, so that it will be spent thoughtfully. Take at least 24 hours before purchasing any goods and do not pay immediately, this will reduce the habit of spending unnecessarily.

,

Read this news too

Your money- How to use Diwali bonus correctly: How much ratio of shopping and investment is right, where to invest the most

Every year most companies give bonuses to their employees on Diwali. This bonus is also a gift of happiness for us and also a chance to improve our financial condition. Read full news …